Canada’s central bank found housing affordability eroded further in the first quarter. The Bank of Canada (BoC) Housing Affordability Index (HAI) showed a sharp jump in Q1 2022. Affordability is now the worst in 3 decades, with the most recent erosion due to rising financing costs. However, this is likely to be temporary as home prices adjust to more expensive borrowing costs. The index will see a short-term increase, but the trend can reverse as early as this year.

The Housing Affordability Index (HAI)

The BoC HAI looks at housing affordability as the basic carrying costs for a home compared to income. Carrying costs are mortgage payments and utilities. Mortgage payments are calculated using a basket of discounted rates, weighted by use. Income is disposable income, which is what’s left after mandatory transfers. The result is the share of income needed to carry these payments, with higher being worse.

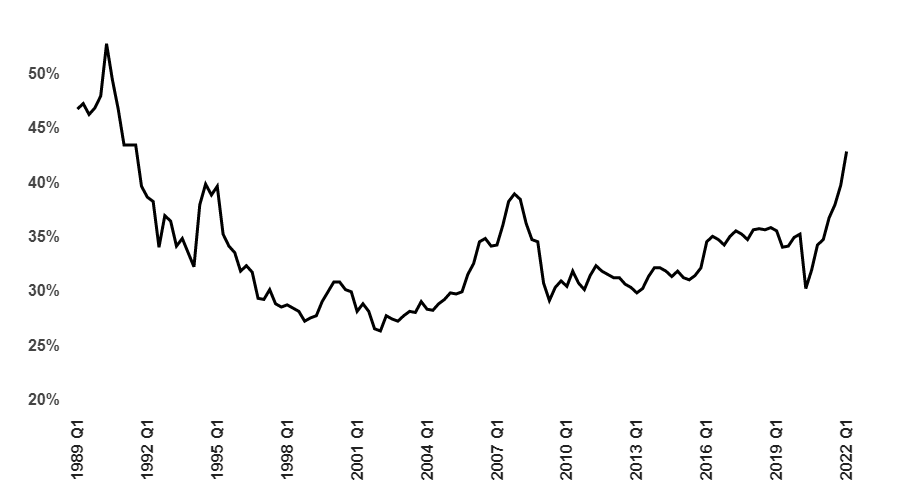

Canadian Real Estate Is The Least Affordable Since The 1991 Bubble

The BoC HAI ripped to the highest level in a generation, and the highest share in 3 decades. The HAI shows a household needs 42.8% of their disposable income to carry a home in Q1 2022. It’s an increase of more than 3 points from the previous quarter and 8.1 points from last year. The HAI hasn’t been this high since Q3 1991, which was the previous peak of the real estate cycle (i.e. the bubble peak).

Bank of Canada Housing Affordability Index

The share of disposable income a typical household needs to carry the mortgage and utilities for a home.

Demographic Distribution Means It’s Harder To Catch Up Without Price Corrections

Age distribution and demographics are important to understand why it’s different this time. Back in the early 90s, the median Canadian was in their early 30s. Today the median person in Canada is a third older — in their early 40s. Half the population in the 90s was below their peak earnings years, making it easier to stomach the costs. This helped to prevent the need for prices to fall as much.

Today, Millennials are expected to reach their demographic peak in the next few years. They’re already past or approaching peak earnings growth, meaning there’s not much income relief. Most of the affordability improvement has to come from falling home prices. They also can’t depend on interest rates to drop 14 points to help alleviate pain and inflate the asset.

Then there’s the whole down payment issue at extended valuations, not factored in by the HAI. The 90s had extreme valuations, with Toronto’s average home sold at 6x the median income. Today that number is closer to 10x, so there’s a considerable gap compared to that period. This isn’t about who had it worse, but the fact that things haven’t improved over the past 30 years.

The BoC HAI is likely to pop even higher over the next quarter but the direction is expected to change fast. Financing costs surged in Q2 2022 while home prices only made a minimal decline in the quarter. This will result in the ratio rising, but more recent activity shows this can change fairly fast. In June, home prices across Canada fell by the equivalent of a third of a median household’s annual income. They didn’t make that drop over the past year, but just in that month. July’s data for Toronto and Vancouver also has experts seeing further national price drops. As early as Q3 or Q4, affordability can start improving — RBC is calling a “historic price correction,” while BMO recently revised their Canadian real estate outlook much lower, expecting big drops in the future.